By Emma Marek.

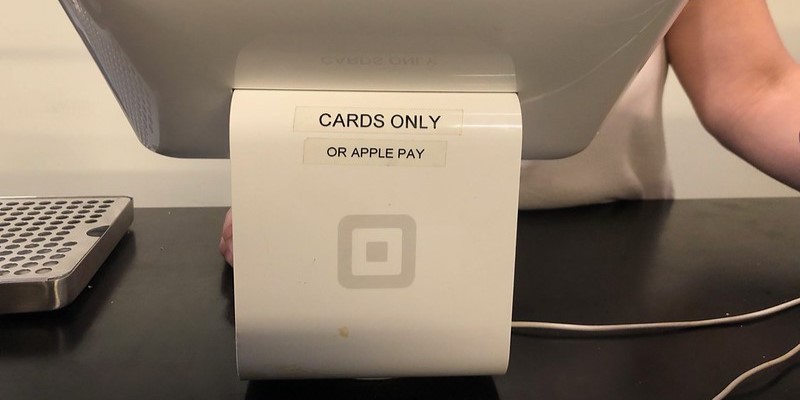

Is cash still king? Or, has a new era of “cashless businesses” dethroned it? Square, a digital payment company, estimates that the number of cashless businesses has doubled in the U.S. since the beginning of the pandemic. Some businesses adopted cashless policies to minimize physical contact during purchases in an effort to slow the spread of COVID-19. Regardless of the medical efficacy of these policies, many businesses have continued to embrace the cashless model for myriad other reasons. Some of the pros of the cashless model include faster transactions, reduced theft and robbery, reduced operational expenses, and improved accounting.

However, cashless models negatively affect consumers that may prefer or rely on cash payments. One of the strongest arguments against going cashless is financial exclusion. The FDIC reports that an estimated 14.1 percent of U.S. Households were underbanked in 2021, meaning the household had a bank or credit union account but lacked adequate access to other financial services such as credit or loans. Further, about 4.2 percent of U.S. households were unbanked in 2021, meaning no one in the household had a checking or savings account at a bank or credit union. Individuals of the unbanked and underbanked populations tend to rely on cash for payments. Although the number of unbanked and underbanked households is decreasing, the existing population faces great difficulty functioning in a cashless society. The same year, the FDIC found that 2.1 percent of White households were unbanked, compared with 11.3 percent of Black households and 9.3 percent of Hispanic households. Because the under and unbanked rates remain higher among minorities, minorities are disproportionately affected by the cashless movement. To address these concerns, an Arizona Representative recently introduced a bill that will require Arizona’s businesses to accept cash payments without penalizing customers.

What is Legal Tender?

Is a business legally obligated to accept cold, hard cash in the first place? It depends.

On each bill of U.S. currency, the words “THIS NOTE IS LEGAL TENDER FOR ALL DEBTS, PUBLIC AND PRIVATE” are printed. Federally, “legal tender” is defined by Section 31 U.S.C. § 5103 as U.S. coins and currency are legal tender for all debts, public charges, taxes, and dues. Under this statute, U.S. coins and currency are a valid and legal means to repay debts to creditors. Under the definition of legal tender in § 5103, businesses do not need to accept your form of legal tender, unless a debt is owed.

So, when are we indebted to a business? As a consumer, you owe a business a debt once you’ve consumed the good or service. To illustrate: you and a friend sit down for breakfast at a restaurant; you order and finish your meals before your server brings you a check to pay. Because you have consumed the restaurant’s goods and services, you owe a debt. Since the private debt may be repaid using legal tender, the restaurant must accept your cash payment. By contrast, if you place an order for a coffee to-go, and you are required to pay in advance at the time of ordering, the cashier is free to refuse your cash payment. Until you consume the coffee, no debt is owed to the business.

Further, Federal law does not mandate that businesses accept legal tender in the form of U.S. coins and bills as payment for goods or services. According to the U.S. Federal Reserve, unless there is a state law to the contrary, private businesses are free to develop their own policies on cash payments.

Several states have taken that liberty. Rhode Island, Massachusetts, and New Jersey—to name a few—have enacted laws requiring their businesses to accept cash payments. Additionally, some cities, such as San Francisco, have passed ordinances to that effect.

Arizona House Bill 2555

In Arizona, there is currently no law that requires a business to accept cash payments. However, the currency Game of Thrones ensues within the State Legislature. Arizona Representative Joseph Chaplik (R) would like cash to be king. Chaplik introduced House Bill 2555 in January 2023. The bill was recently passed by the Arizona House in February 2023, and is on its way to the Arizona Senate. The Bill would require all retail businesses with physical locations in Arizona to accept coins and cash as payment for goods and services. Additionally, businesses may not charge customers a fee or penalty for using cash and may be subject to monetary damages for violating the law.

If the Bill becomes law, issues will very likely arise from the “retail” requirement; only retail businesses, as classified under A.R.S. § 42-5061, would be subject to the cash mandate. The statute defines retail as the business of selling tangible personal property. Confusion around the proper classification may arise, especially when a business’ operations fall under multiple classifications. See generally SWAT Training Facilities LLC v. Arizona Dept. of Revenue, 490 P.3d 378 (Ariz. App. 1st Div. 2021) (discussing retail nature of membership benefits despite shooting range’s general amusement classification).

Under Massachusetts’ equivalent cash payment statute, a debate has arisen over how to apply the law. The statute prohibits retailers from discriminating against cash buyers by requiring credit card payments. In 2022, Fenway Park went cash-free, but added kiosks to allow customers to load their cash onto prepaid Mastercard debit cards, which could be used to make purchases for concessions within the stadium. The Massachusetts Attorney General endorsed the kiosks as an acceptable workaround to the law. Whether such a workaround would pass muster under the proposed Arizona law is yet to be determined. It is questionable whether smaller businesses would be able to offer such an accommodation if faced with a cash mandate. Further, even if it allows a business to avoid an enforcement action, prepaid card kiosks and other workarounds are not a solution to the financial exclusion problem and do not ease access to other banking, credit, and loan services.

Conclusion

It remains to be seen whether House Bill 2555 will be enacted and how it might be enforced in the State of Arizona. Regardless, the Bill certainly illuminates the ongoing debate around the role of tangible and intangible forms of currency and the role of cash in our modern society.

Emma Marek is a 2L Staff Writer from Lake Oswego, Oregon, interested in Corporate and Securities Law. Before law school, Emma studied Political Science and Economics at Texas Christian University in Fort Worth, Texas. Go Frogs! In her free time, Emma enjoys hot yoga, distance running, and movie nights with her family.